Whether crop prices are high or low, it’s wise to watch balance sheets closely and check how you stack up to performance benchmarks across the industry. With grain prices trending lower, the focus for many has shifted from expansion to maintaining what they currently have. This holding position may be prudent. However, production must continue and new opportunities will present themselves despite the fact that you’re managing finances with a sharp pencil.

At Farm Credit Mid-America, we encourage growers to keep an eye not only on expenses, but also on asset utilization and fixed costs as they relate to GFI (gross farm income). Consider various fixed cost ratios using capital interest, principal payments and land rents as a percent of GFI to measure how effectively you are utilizing assets.

Especially when margins are tight, farmers need to dig deep into how fixed costs and inputs relate to production capacity. We’re talking about utilization of equipment and fixed assets. Are you getting the right kind of utilization? Are you over-equipped? Are you under-equipped? Do you have more labor than what you really need? What inputs give you the best value? Capital is a finite source, so every dollar allocated to an underutilized asset is a dollar that can’t be deployed to liquidity or working capital when needed.

Evaluating your balance sheet isn’t just about the information or analysis Farm Credit uses to approve loans. Fiscal awareness is valuable for any grower who is trying to stay efficient during times of low crop prices and tight margins. In 2015, low commodity prices means there will be farmers who have to operate at a loss for a year or two. The more knowledge you have of your cash burn rate (cash required to cover shortfalls in cash flow), the more confident you can be of how long you can operate at a loss until crop prices turn around. Understanding your burn rate will also help determine what new opportunities you can take advantage of. The key thing to remember is you can’t burn what you don’t have.

How do you stack up?

Working with operations of all shapes and sizes has given us experience seeing what success looks like for each operation, as well as how individual farms can start to slip into financial trouble. In addition to looking at each farm’s profit and loss numbers, we can benchmark farms and see how they compare against the key financial metrics of successful farms.

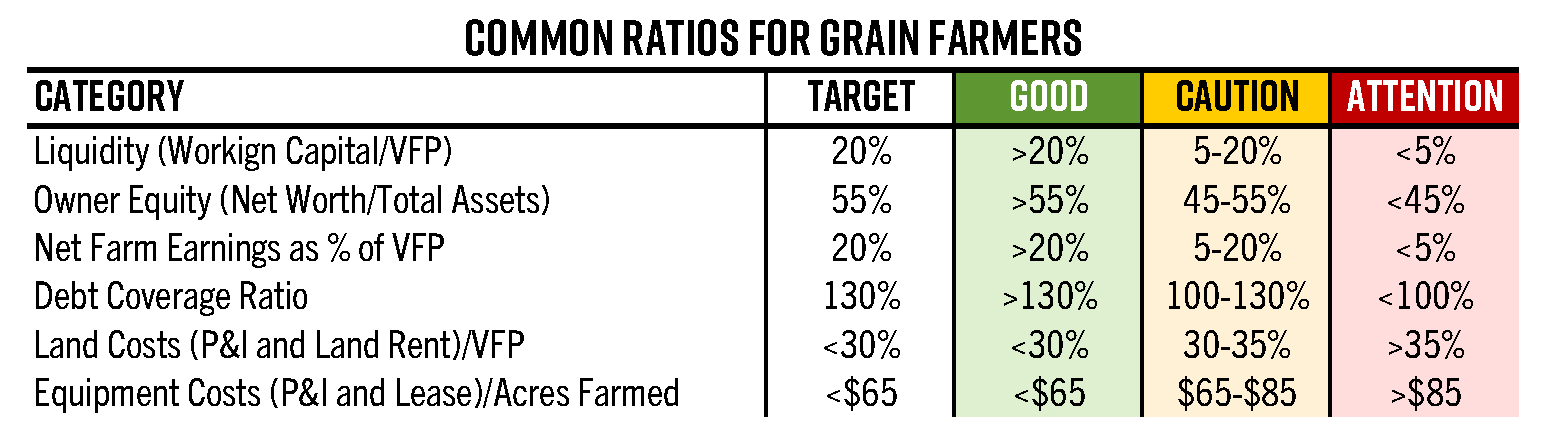

The chart below shows a few common financial ratios for grain farms. These are guides and not absolute measures. Each farming operation is unique, but being significantly outside these measures will often create challenges.

Working capital (current assets minus liabilities) is a measure of the amount of funds available to meet the payment of all current liabilities. Working capital compared to VFP (value of farm production) relates the amount of working capital to the size of the operation. The higher the ratio, the more liquidity the farm operation has to meet current obligations and, more critically, how much adversity can you withstand before asking your lender for additional operating funds. Another way to think of this is working capital per acre, which equates to commodity price and bushels per acre and eventually how you develop your risk management plans. The ratio varies across farm types and other farm characteristics.

Find your balance

When grain prices drop, growers are motivated to renegotiate cash rents, but don’t want to lose land and production capacity. Many are relying on liquidity to hold on and produce at a loss until the grain market or rental market adjusts. But you have to ask tough questions. If you’re burning working capital at a rate of $50 an acre per year, for example, how long can you withstand that before you have to go back and renegotiate?