Are you using your tax return to track your operation’s expenses? If so, you’re probably not getting the full picture. Most farmers are good at tracking the money that comes in and goes out, with the goal of filling out tax returns and farm income statements. However, there are non-deductible costs that won’t appear on any end-of-the-year tax forms, but will still affect your bottom line. One of the largest hidden costs on your balance sheet can be your principal payments and asset efficiency.

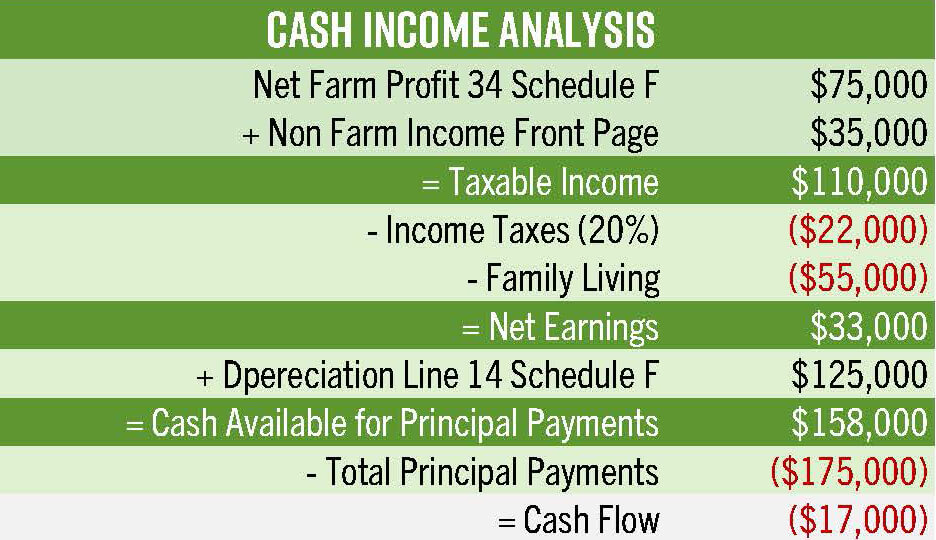

All term debt principal payments are paid from cash left over after living and income taxes are paid. What does that mean? Let’s look at a simple calculation using just the schedule F from the tax return. We will keep it simple and assume cash accounting:

In this example, the operation is showing taxable income and net earnings after income taxes and living is paid, but cash flow is negative. Lenders refer to this type of calculation as a Debt Coverage Ratio, or DCR. This negative cash flow transfers directly back to the working capital on the balance sheet. Additionally, if you choose to pay cash for any capital assets in the year using this example, 100 percent of the cash used for the purchase reduces working capital.

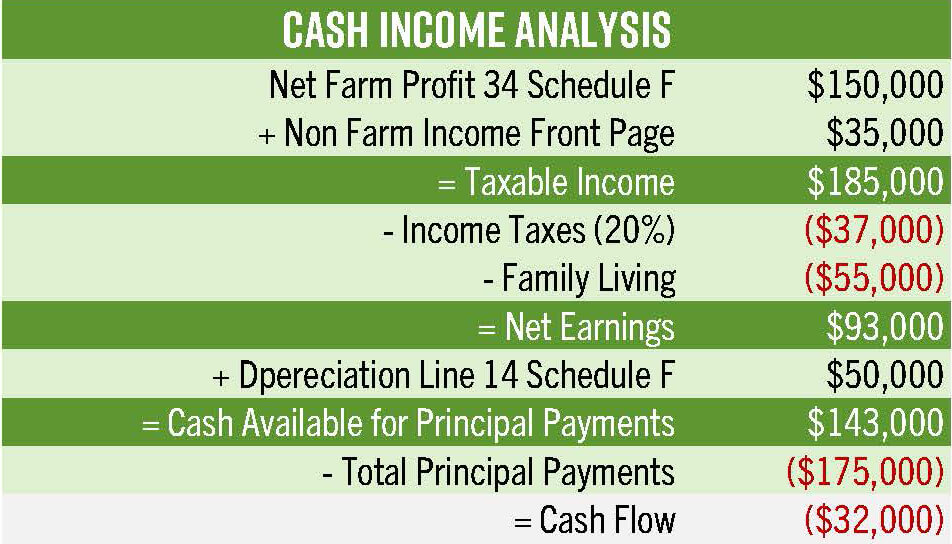

Be wary of the Section 179 trap. If you purchased a new tractor and chose to fully depreciate it in the purchase year using the 179 Deduction, but borrowed money to buy the tractor, you may have reduced your ability to manage your tax expense the following year. Using the example above and assuming $75,000 of section 179 depreciation was used when the tractor was purchased, you gave away your depreciation tax shelter and now must generate enough net earnings (after tax income) to cover the principal payment on the loan going forward. The table below shows impact on cash flow for the following year assuming the only difference is the lower depreciation and the resulting tax expense.

If you’re noticing your working capital position or margins declining, take care to assess the above situations. This situation can be a key indicator something isn’t adding up in your operation’s finances, and the culprit could be your principal payments and asset efficiency.